The National Customs and Tax Authority (NAV) has recently published its annual report – something of a tradition now – which summarises its activities over the past year. Looking through the many statistics, the picture that emerges is that the efficiency of NAV audits has increased in recent years.

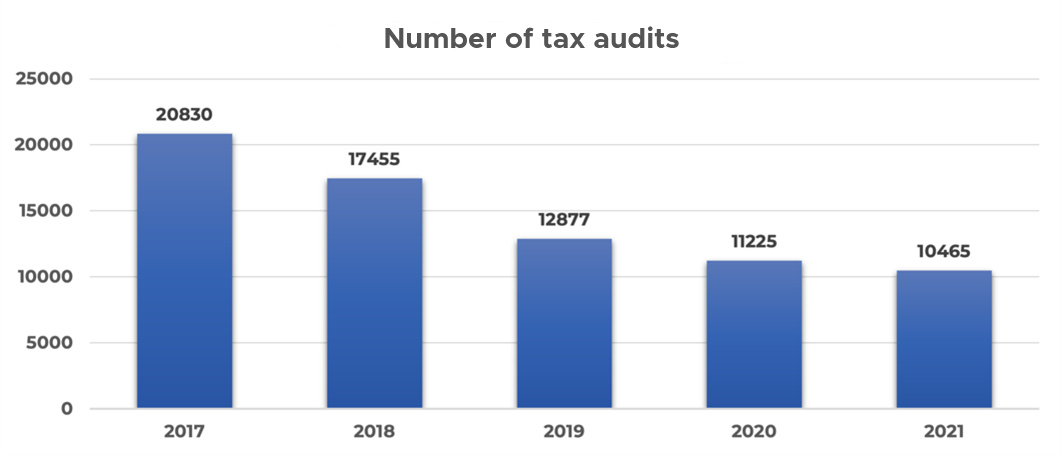

Decreasing number of audits

As can be felt in everyday life, the number of audits carried out by the tax authority has fallen significantly in the last five years: The NAV now typically knocks on your door only when it feels it has something to find. This downward trend started in 2017, when the number of tax audits suddenly dropped from 36,000 to 20,000. But since 2017 the number of NAV audits per year has also essentially halved.

It should be noted that the downward trend only applies to tax audits, not to compliance audits, the number of which has not changed significantly over the last 5 years.

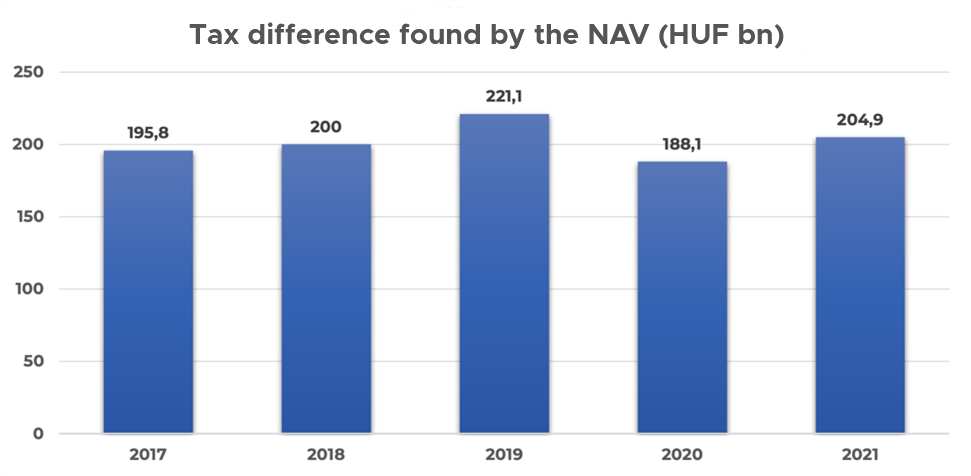

No change in the tax difference discovered

According to NAV statistics, roughly one in eight audits – the vast majority of which concern VAT – ends with a finding. As a result of these findings, the NAV’s audit department discovered a net tax difference of HUF 204.9 billion in 2021. Looking at similar figures for previous years, there is no significant change in this respect, with the amount of tax difference discovered in 2021 roughly the same as the average of the last 5 years. However, this also indicates that the NAV has become more efficient, as it has been able to discover the same tax difference by launching significantly fewer tax procedures.

However, the picture is slightly overshadowed by the fact that only 20.9% of the tax difference was deemed recoverable by the tax authority, the lowest rate in the last 5 years.

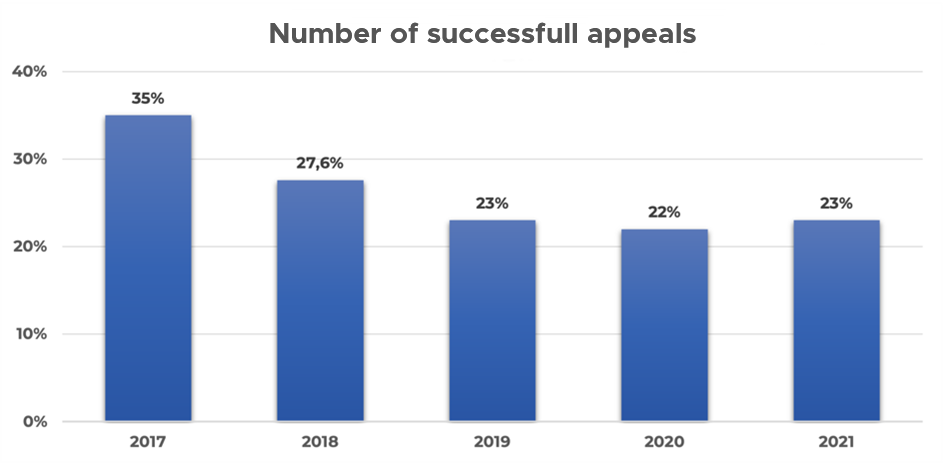

It is becoming increasingly difficult to successfully fight the NAV

Over the past decades, taxpayers apparently realised that it paid to fight against the NAV’s findings: over this period the taxpayers’ success rates improved almost continuously. However, this trend has reversed in the last 5 years. In 2021, the NAV Directorate of Appeals decided on a total of 1,796 appeals against first-instance decisions in the field of audits, of which 23% were successful. While this rate is broadly in line with the data of the last 2 years, it is significantly lower than either the 2017 or 2018 figure. As for the number of lawsuits against the tax authority, last year 493 audit cases were adjudicated, of which one in five were favourable to the taxpayer.

It seems that not only is the tax authority more selective now in the subjects of its audits, but it is also increasingly prepared to defend the results of its audits. It is therefore becoming more and more important for taxpayers to seek the most effective professional assistance in a tax dispute and to consciously prepare at the outset of the dispute for the steps that will follow.